Where Euro Rates Volatility Has Outperformed the US Dollar

Interest rate rises triggering opposite effects in the euro versus the dollar volatility market have created new investment opportunities.

The traditional narrative about US rates volatility has been turned on its head

Global institutional investors are exploring the euro rates volatility market to capture a unique opportunity

A pullback from US MBS players combined with greater hedging in the euro market have upended the rates volatility market

Euro rates volatility has eaten away at the US dollar’s dominance in offering the most attractive volatility carry opportunities after higher interest rates caused more hedging demand in Europe and less in the US amid structural changes in the mortgage market.

The traditional narrative dictated that only US dollar volatility was worth trading as the US mortgage-backed securities (MBS) market has long driven a steady demand for volatility to hedge against pre-payment risk by US homeowners.

Mortgage servicers buy USD interest rate options (e.g. swaption receivers) to hedge their cash flows, which disappear if mortgage-holders prepay their current home loans and refinance at lower rates. When rates hit rock bottom in the wake of the pandemic, a massive refinancing wave occurred among US mortgage borrowers. When rates started rising again in 2022, there was no incentive for homeowners to refinance so the pre-payment risk largely subsided, resulting in a pullback in hedging demand from MBS servicers.

Carry strategies in rates volatility involve selling interest rate options (delta-hedged swaption straddles) to capture the spread between implied volatility and realized volatility. Implied volatility typically trades higher than realized volatility at shorter expiries, which have more gamma.

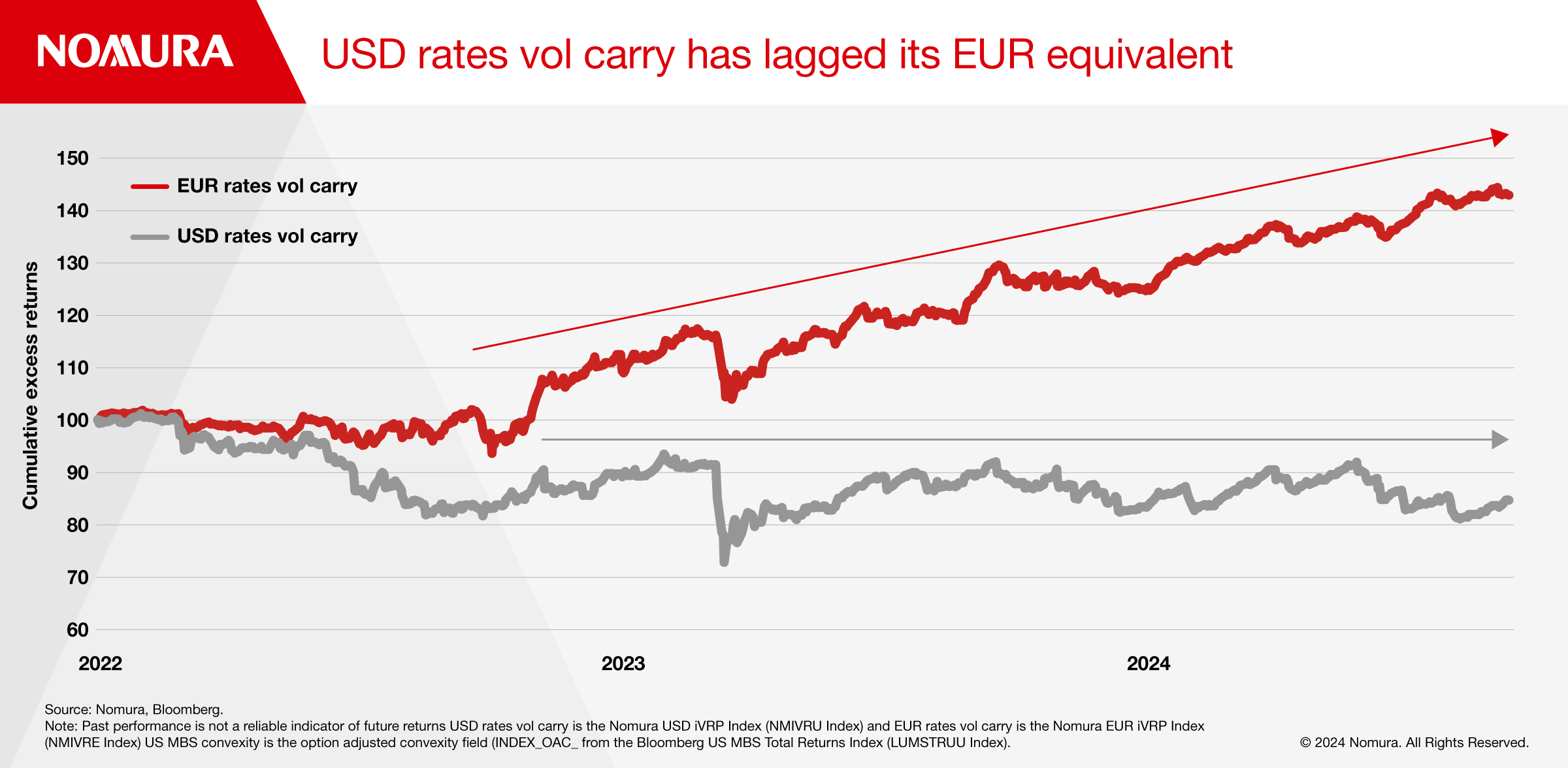

Demand for swaption gamma increases the level of implied volatility relative to realized volatility, making volatility carry more attractive. Chart 1 shows how USD rates volatility carry has stagnated since 2022 while its EUR equivalent has powered ahead.

Chart 1: USD rates vol carry has lagged its EUR equivalent

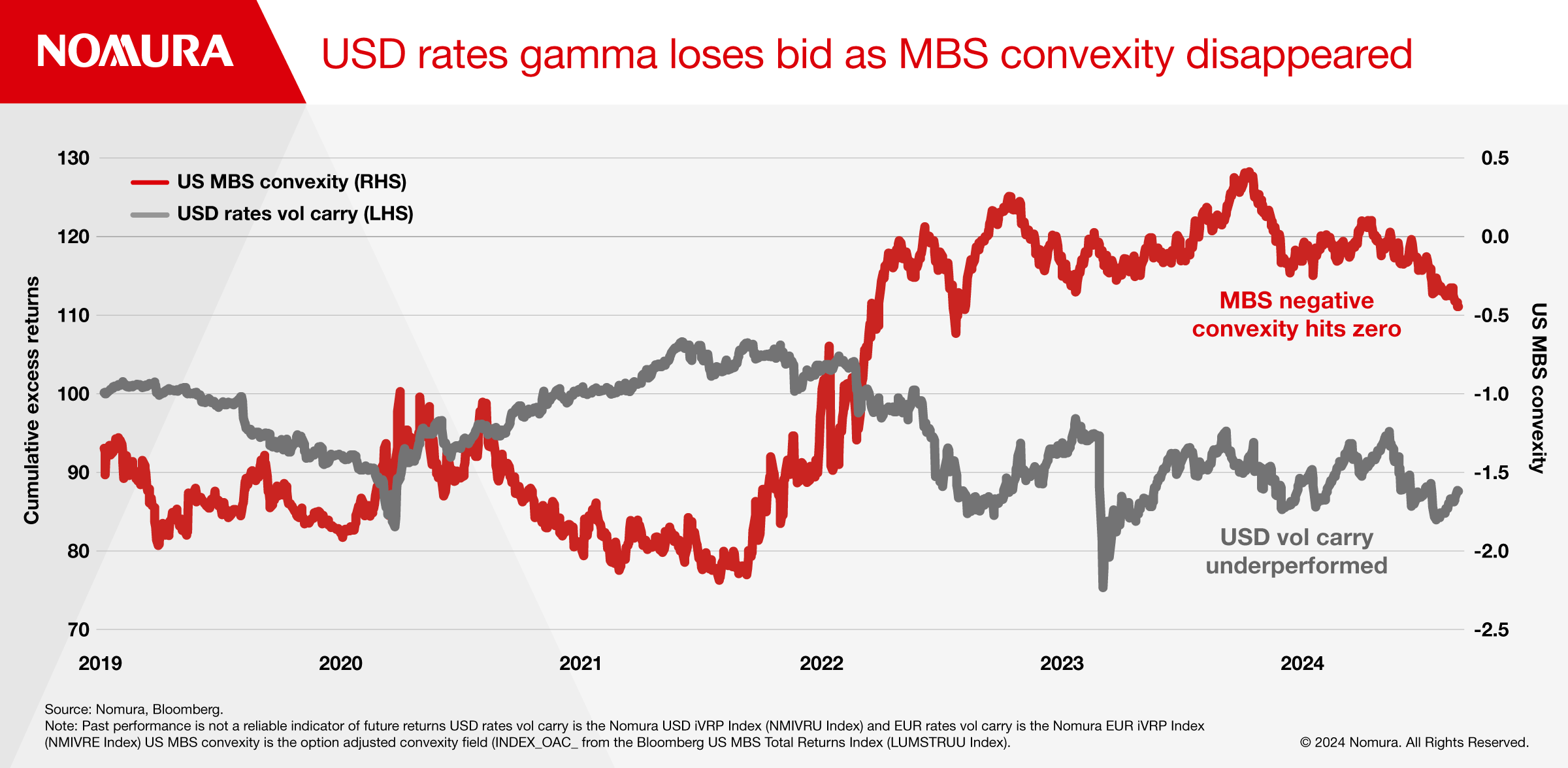

Tony Morris, Global Head of Quantitative Strategies at Nomura says that for many years, the US MBS market was a poster child of negative convexity, in other words, the characteristic that duration would get longer as rates increased, which is the opposite of normal convexity in vanilla bonds. This negative convexity, like “short gamma” in derivative terms, arises from the prepayment optionality that homeowners are long but MBS investors are short.

“When this structural demand to hedge prepayment optionality fell away, USD rates gamma was less bid, making it less attractive for volatility carry,” says Morris.

These market dynamics led to the US MBS benchmark running an average option-adjusted convexity (OAC) of about -1.5 for decades, while the OAC of a vanilla bond index of similar duration would be positive but close to zero.

In 2022 for the first time, the OAC of the US MBS market vanished, going from -1.5 to zero, as shown in Chart 2. This happened as a direct consequence of the rise in US interest rates.

Given the exceptionally low interest rates in 2020-2021, US homeowners had refinanced in large size, such that the overwhelming majority of outstanding MBS had coupons of 3% or less. By the end of 2022, the typical new-issue MBS coupon was over 6%.

In other words, the receiver swaptions that MBS investors (and mortgage servicers) were short were about 300 bps out of the money. With the exercise of prepayment optionality so unlikely, negative convexity shrank to zero.

In swaption terms, a deep-out-of-the-money receiver would have very low gamma. With little short gamma risk in their positions, as US homeowners were very unlikely to prepay their 3% mortgages when current mortgage rates were near 6%, mortgage servicers have had little interest in paying to hedge this risk, and thus a big source of demand for USD interest rate volatility decreased markedly.

“It is not surprising that volatility carry in US dollar swaptions has stagnated, as mortgage servicer demand for rates gamma to hedge prepayment optionality was key to elevating implied relative to realized volatility,” says Morris.

Conversely, the opposite dynamic has been present in the euro volatility market where firms started hedging again.

Prior to 2021, EUR interest rate volatility was subdued amid a prolonged period of ultra-low rates. Complacency had settled into the market and relatively few market participants seemed focused on buying gamma, or even staying flat, as long-term short positions accumulated.

But as inflationary pressures kicked in and the ECB began hiking in 2022, the market rediscovered interest rates could be volatile. Massive volatility buying ensued to hedge positions, creating a widening in the spread between implied and realized volatility.

As a result, large parts of the EUR rates volatility surface started trading higher than USD equivalents for the first time in market memory.

If that wasn’t enough, regulatory changes under the Solvency II framework encouraged pensions and insurers towards the market. In order to comply with the new rules, some firms had a particular need to buy swaptions to address asset-liability mismatches.

“The confluence of these different factors has triggered interest in euro rates volatility from a range of global institutional investors including endowment funds,” says Steven Loeys Head of QIS structuring at Nomura. “Investors can have different objectives, ranging from pure carry harvesting to adding more balanced or defensive overlays, and the flexibility of our platform allows us to cater solutions to their specific needs.”

While these dynamics are still at play, much lower USD interest rates would trigger a return of negative convexity and mortgage servicers would probably increase gamma hedging. Even if rates stay near current levels, over time the accumulation of new mortgages at close to current levels should increase negative convexity, albeit at a gradual pace. As for EUR gamma demand, the new regulatory environment suggests it is here to stay.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction.