We expect 2023 to bring into focus a nascent recession, with pronounced weakness across a broad range of economic indicators

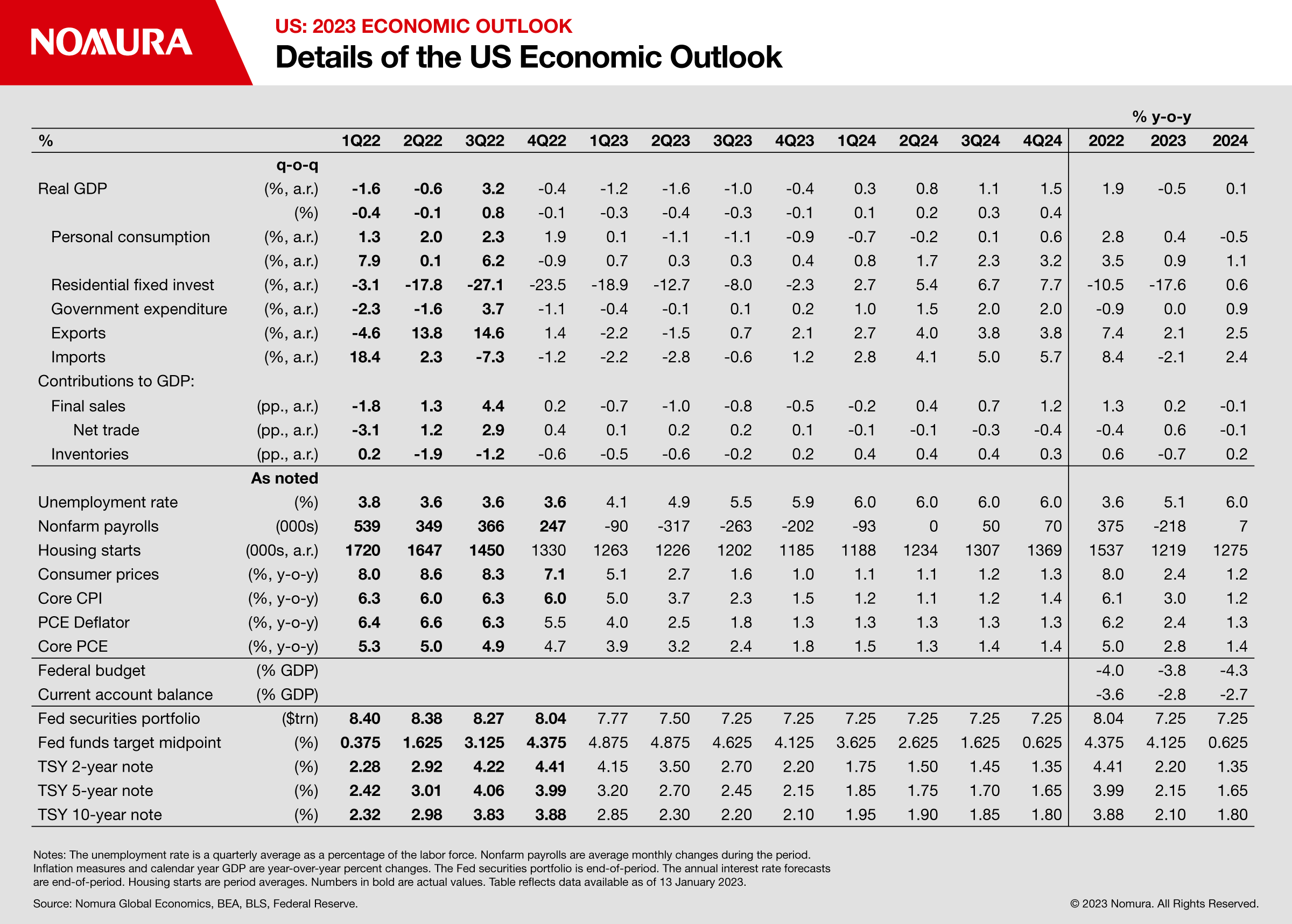

We expect 2023 to bring into focus a nascent recession, with pronounced weakness across a broad range of economic indicators, resulting in real GDP falling 1.1% on a Q4/Q4 basis.

As inflation shows signs of easing, the Fed will likely raise rates only twice, by 25bp in February and March, to a terminal rate of 4.75-5.00%.

Inflation will likely underperform in H2 as labor market conditions weaken considerably – with a peak unemployment rate of 6.0% – resulting in a gradual pace of rate cuts starting in September.

Policy that provided tailwinds during the pandemic is now causing headwinds; that shift will likely prolong the overall downturn. More resilient consumer activity relative to our expectations not only poses upside risk to growth, but also potentially to policy rates.

The Outlook for the Real Economy and Labor Market

We continue to believe the economy is in the early stages of recession

Economic

growth momentum continues to rapidly wane, and we believe the economy is in the

early stages of entering a recession as of Q4 2022. The housing market downturn

has accelerated as home sales and prices are now both falling rapidly. The

industrial sector appears close behind, due to a series of synchronized

negative shocks including a stronger dollar, collapsing external growth,

saturated domestic goods markets and higher interest rates.

More

broadly, a number of key economic indicators used for dating recessions by the

National Bureau of Economic Research (NBER) have begun to soften. Faltering

business confidence, tightening lending standards and waning loan demand will

all likely weigh on business investment across both structures and equipment.

Rates-sensitive consumption has started to slow, including in autos, despite

pent-up demand acting as a modest buffer.

In 2023, we

expect the domestic economic slowdown to broaden and intensify as the Fed remains

aggressive, financial conditions tighten further, the labor market weakens and

consumers pull back more meaningfully on spending. Service consumption has

benefited from a gradual rotation away from goods, but that modest tailwind

will likely falter as job losses start in early 2023. Excess savings and

state-level transfer payments have likely underpinned spending, but support

from both factors is unlikely to be sustained. In addition, momentum for

COVID-sensitive services has continued to trend lower in recent months,

consistent with widespread weakness across major service business surveys.

We continue

to believe the initial pullback in economic activity will be relatively mild,

in part reflecting strong initial conditions for households relative to

previous downturns. However, monetary and fiscal policy headwinds into the

downturn – in contrast with the historical reaction function and

reflecting the unusual nature of the current macroeconomic environment

– will likely prolong the recession. In many ways, we believe the upcoming

recession will be a function of the Fed’s efforts to return trend inflation to

2% sustainably.

Altogether,

we expect real GDP growth of -0.5% y-o-y and +0.1% y-o-y in 2023-24 (-1.1% and

+0.9% Q4/Q4), respectively. We expect five consecutive quarters of economic

contraction from Q4 2022-Q4 2023, followed by an only-muted recovery.

Labor

markets in 2023 – the elephant in the room

Exceptionally

tight labor markets remain inconsistent with the Fed’s 2% inflation objectives,

in our view. In 2023, we believe the focus will shift to how quickly labor

market momentum continues to soften, including the timing and duration of job

losses, along with the ultimate destination of the unemployment rate in this

cycle. It is also important to see how quickly wage growth will decelerate

as non-housing core service prices, a key inflation metric, is considered as

being closely tied to wage growth.

At the

moment, labor markets remain strong, but forward-looking indicators have begun

to soften. Monthly job gains in cyclically sensitive industries have slowed

notably, continuing jobless claims are steadily rising, the Conference Board’s

labor market differential has eased from recent highs, and gross hires and

quits have started to move lower as firms and workers become more cautious.

In terms of

ordering, we expect an initial slowdown in hiring – the easiest lever for

most firms to pull – before reductions in job openings and outright

layoffs. Layoffs remain concentrated in the tech sector, but we expect

headcount reductions to soon spread to construction and manufacturing

(reflecting challenges in the housing and industrial sectors, respectively)

before broadening to the service economy in 2023. Labor hoarding during the

pandemic recovery, in an environment of severe labor shortages, could result in

a discontinuous increase in layoffs once firms shift their expectations to a

persistent contraction in economy activity. Altogether, we expect the

unemployment rate to rise to close to 6% by end-2023, where it will likely stay

through 2024.

A soft

landing is possible, but remains unlikely

For the

economy to achieve a soft landing – inflation moving lower without a recession

– we believe a few factors will be required, all of which have shown scant

evidence of coming to fruition.

First, the

easing of labor market tightness would need to come overwhelmingly from

declining job openings as opposed to rising unemployment. Second, a more

sustained recovery in labor force participation (labor supply) would likely be

required to ease wage pressures without a meaningful increase in the

unemployment rate. However, in recent months,

the labor force participation rate (LFPR) has stable around its 2022 average,

and underlying data suggest the preponderance of workers that have not returned

relative to pre-pandemic levels are retirees, who show few signs of returning

to the labor force.

Third, the

national inflation conversation will likely need to dramatically improve.

However, similar to labor supply, the percent of workers hearing “bad news”

about high prices, and the percent of small businesses reporting inflation as

their “single most important problem,” have shown few signs of improving.

Persistent inflation attention from households and businesses, all else being equal,

risks keeping inflation expectations elevated and, we believe, requires a more

forceful Fed response.

Risks to

the economic outlook

Considering

our below-consensus economic outlook, we see a few upside risks to growth.

Specifically, moderating inflation – led by the goods sector – could

result in stronger real wage growth. That said, weak labor productivity growth

in recent quarters suggests a prolonged period of strong real wage growth is

unlikely.

In addition,

we assume the impact of excess savings on consumer spending will continue to

gradually diminish, but a more prolonged boost to consumption is possible.

Finally, if long-term interest rates fall faster than we assume, it could

result in an earlier boost to interest-rate sensitive consumption, particularly

housing.

On the

downside, the depth of the recession will likely be proportional to how

entrenched inflation proves to be. Persistently high or more entrenched

inflation could result in an even more aggressive Fed response, resulting in a

deeper contraction. Moreover, while financial conditions have tightened in a

relatively orderly way so far, an abrupt repricing of risk could result in a

nonlinear response, particularly in corporate credit markets, which could

result in a deeper recession.

The Outlook for Inflation

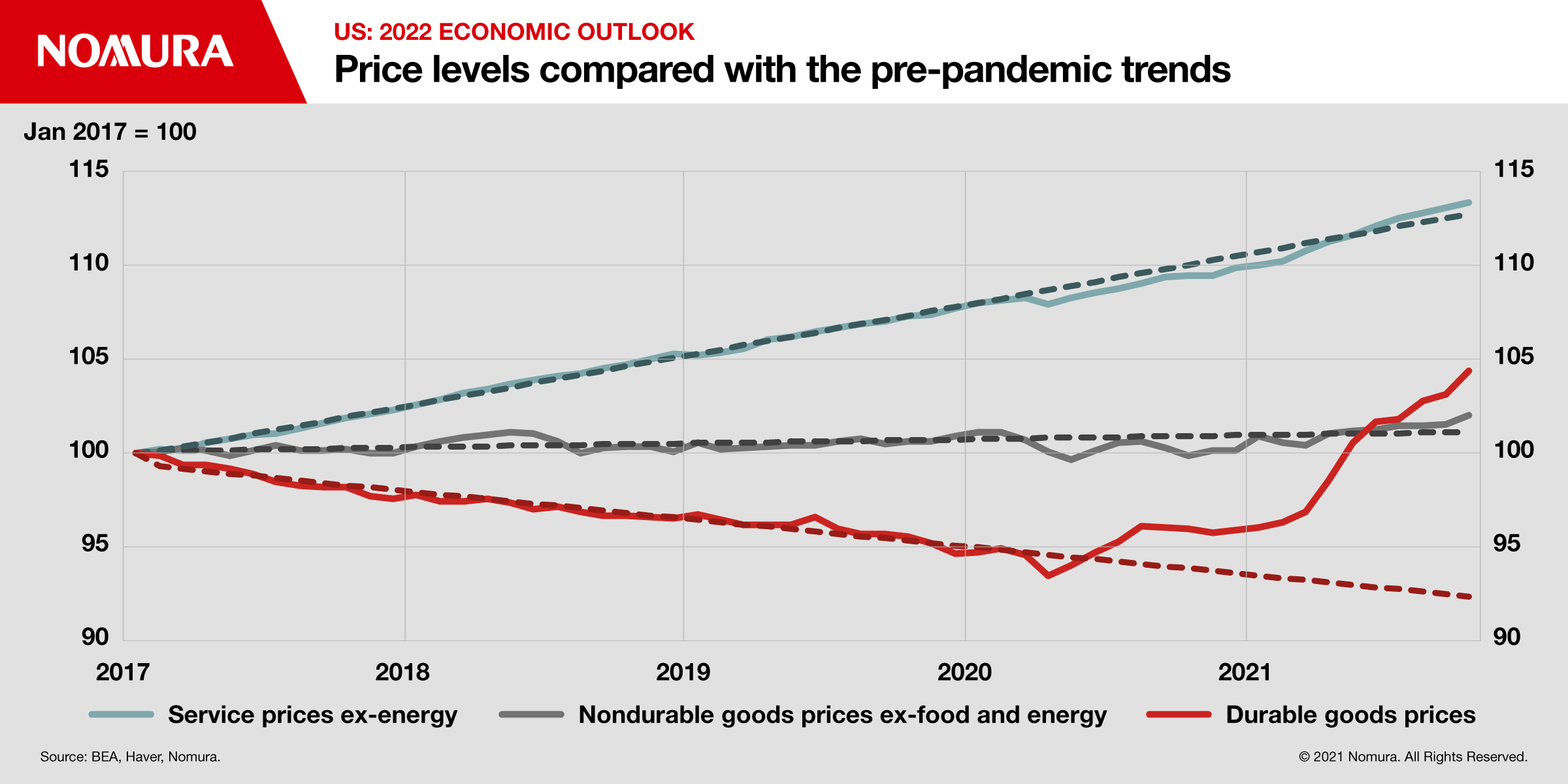

Goods price

disinflation is finally taking hold, but services remain problematic

After

accelerating at a brisk clip, inflation has finally started to show signs of

moderation. In particular, there is growing evidence of easing pressures on

goods prices as supply chains continue to normalize. For example, shorter

supplier lead times and the lagged impact of a stronger US dollar are now more

clearly weighing on import prices. In addition, shipping costs have moderated,

and retailers’ inventories have been replenished.

However, the

main driver of inflation has been shifting toward core services, which tend to

be sticky and more closely tied to labor markets. We expect a tug of war

between lowering goods prices and persistently high service inflation to

continue during the first few months of 2023. That said, considering goods

prices are volatile and prone to external shocks, we believe service prices –

and hence labor markets – are a more important determinant of trend underlying

inflation.

The

outlook for core services inflation

In terms of

m-o-m core PCE inflation, which is the most relevant inflation metric for the

near-term monetary policy outlook, we decompose core PCE service prices into

three groups: rent/owners’ equivalent rent (OER), healthcare services and other

services as those groups appear to follow different price dynamics.

For rent/OER

inflation, our modal forecast suggests m-o-m rent inflation will likely start

to decelerate sometime in Q1 2023, based on the historical lead-lag

relationship between the official and private rent data.

Healthcare service prices – accounting for more than 15% of the core PCE

price index – will likely become increasingly important for the near-term

monetary policy outlook. Specifically, Medicare’s payments for outpatient

hospital care are updated in January each year based on “market baskets”

of goods and services that medical providers purchase, suggesting we will

likely see the lagged impact of past wages and goods price inflation on

Medicare hospital prices in early 2023.

We think that core service inflation excluding rent-related components

and healthcare is closely correlated with wage growth and as the economy slows,

we expect this component to moderate gradually. We have already seen some signs

of decelerating wage growth, supporting our view that core service inflation

excluding rent/OER and healthcare will moderate substantially in 2023. Overall,

we expect y-o-y core PCE inflation to reach 2% by the end of this year.

Risks and

uncertainty around our inflation outlook

That said,

there is a great deal of uncertainty and risks around our inflation outlook.

Goods prices could easily become inflationary forces considering increasing

vulnerability of supply chains to external shocks such as geopolitics,

de-globalization and climate change.

There is the possibility of underestimating overarching macro factors.

Specifically, persistently strong wage inflation despite some cracks in labor

markets indicates the risk of a wage-price spiral. Recent labor disputes in

certain industries underscore that concern as the cost of living might be

starting to become entrenched in the wage-setting process.

The Outlook for Monetary and Fiscal Policy

A

discovery process for the Fed’s reaction function in early 2023

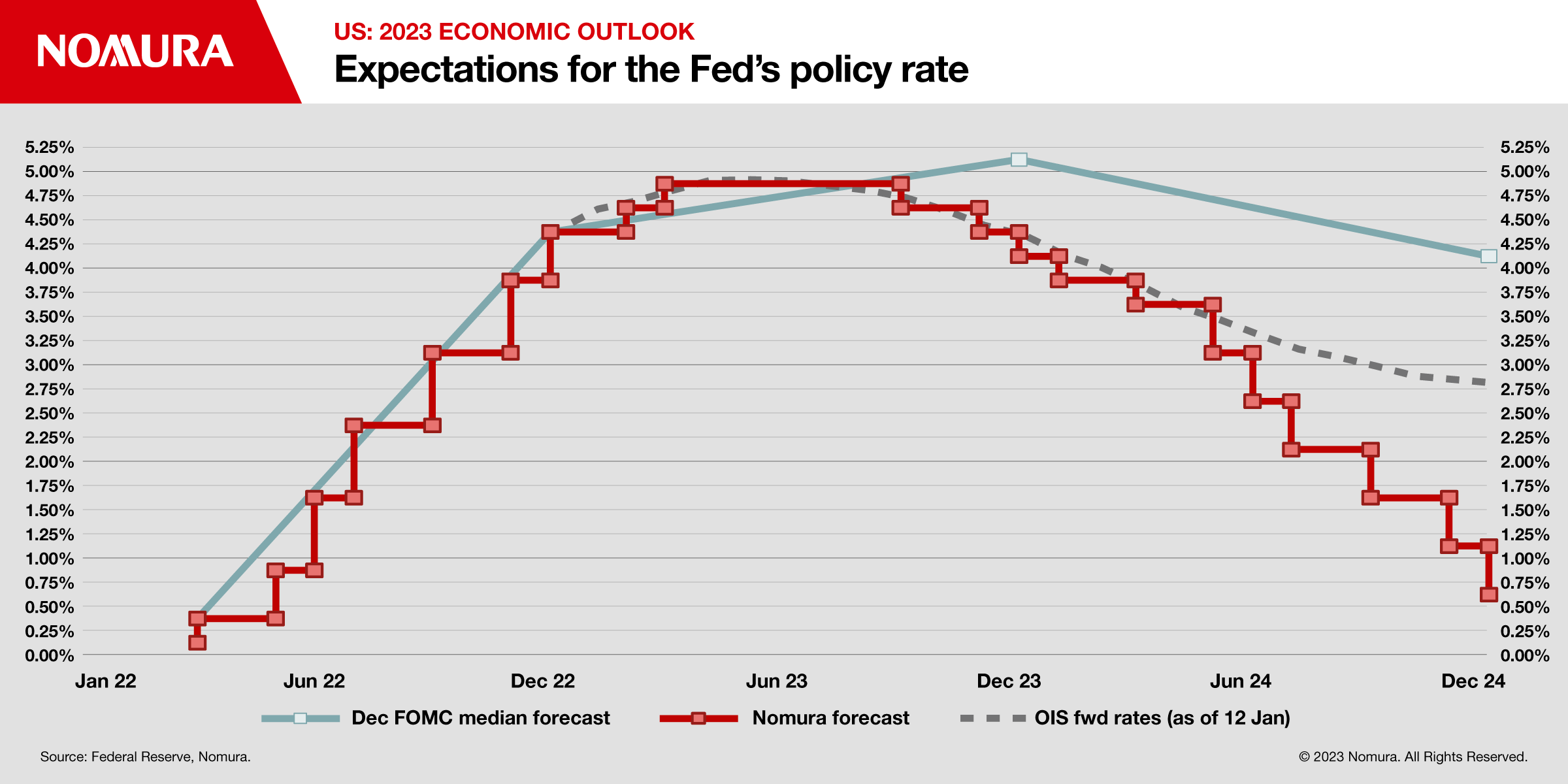

2022 was characterized by the most rapid rate hiking cycle in modern memory as Fed participants sought to catch up with persistently elevated and increasingly entrenched inflation. With the Committee downshifting to a 50bp rate hike in December, policymakers are now beginning discussions regarding the necessary criteria for both slowing the pace of rate hikes further, and eventually pausing. Chair Powell’s comments at the December FOMC press conference suggest a preference for slowing to 25bp hikes in February as the FOMC seeks to ascertain the appropriate level of restrictive rates

In our modal outlook, we assume Fed participants remain focused on the trend of realized m-o-m core PCE inflation and relevant trend inflation measures such as the median and trimmed-mean PCE to determine when to stop raising rates, continuing hikes until the underlying trend of m-o-m core PCE inflation drops below 0.3%. Accounting for our inflation forecast, we believe this will result in 25bp hikes in February and March to a terminal rate of 4.75-5.00% despite our recession expectations.

The

threshold for rate cuts and our expectations

Tying

together our recession expectations, the labor market outlook and inflation

forecast, we believe m-o-m core PCE inflation will drop below 2% on an

annualized basis starting around mid-2023. Against that backdrop, with the

economy mired in recession and an unemployment rate quickly approaching 6%, we

expect Fed participants to begin cutting rates gradually by 25bp per meeting

starting in September. The slower initial pace of rate cuts will likely be

motivated by concerns of a rebound in inflation, but if it becomes clear core

PCE inflation will undershoot the Fed’s 2% target in 2024, we expect the pace

of rate cuts to accelerate to 50bp per meeting in Q2 that year.

Similar to

the reaction function for pausing rate hikes, we see elevated uncertainty over how

the Fed will respond to eventually cutting rates. Almost all Fed participants

remain reluctant to publicly consider rate cuts in 2023, likely for fear of

easing financial conditions undoing their work to tighten this year. Moreover,

while participants and the Fed staff have become more pessimistic about

avoiding a recession, most participants still suggest their modal outlook

includes sub-trend but positive real GDP growth. Once a recession becomes

clear, and inflation underperforms, participants will likely coalesce over a

gradual initial pace of cuts, especially considering that as inflation falls,

the Fed’s policy rate will mechanically become more restrictive in real terms.

US Economic Outlook: Expectations for the Fed's policy rate

Financial

conditions, financial stability and volatility

Financial conditions have tightened notably in 2022 as the Fed’s hawkish

pivot took hold. In 2023, we expect ongoing tightening – including

further declines in equity prices, wider corporate credit spreads and increased

difficulty in small business access to credit – as the Fed raises rates

further and holds them at a restrictive level despite an ongoing recession.

Once inflation starts to persistently underperform in mid-2023, and the Fed

signals rate cuts are likely, financial conditions may ease somewhat, but the

initially slow pace of easing could limit any positive impulse.

The Fed

and political pressure in 2023

We believe

the Fed in 2023 will come under some of the most intense political pressure it

has faced since the 1980s. Already, some members of Congress have sought to

discourage the Fed from further rate increases due to concerns over the labor

market. While the White House has largely maintained its distance and continues

to promote Fed independence, the criticism from Congress will likely intensify

next year as job losses start. Powell’s hawkish comments so far have been

easier to maintain in an environment with historically low unemployment rates,

but that will likely become more difficult once the labor market deteriorates.

His semi-annual testimony before Congress in February will likely be

contentious.

That said,

we do not believe the Fed will respond meaningfully to political pressure.

Powell and other Fed participants have been clear that long-run labor market

health depends on low and stable inflation, and we also believe Powell has

become conscious of how history will view him in a high-inflation environment.

Repeated emphasis on former Chair Volcker’s experience suggests a lower

likelihood he will settle for a persistently higher level of inflation without

first going through an economic downturn.

The

outlook for fiscal policy

A return to divided government in 2023 – Republicans and Democrats

holding very narrow majorities in the House of Representatives and Senate,

respectively – will likely usher in a period of elevated fiscal policy

volatility and close the door on meaningful fiscal stimulus during the latter

part of our expected recession.

Similar to monetary policy, we believe divided government in 2023 will

result in a lack of fiscal support during the economic downturn. Republicans

face few incentives to provide cooperation ahead of a pivotal 2024 presidential

election, especially in an environment where many politicians continue to

debate just how much of current unwanted inflation stems from excess pandemic

fiscal support, and how effective additional fiscal support would be in a

high-inflation environment. All else being equal, the lack of fiscal support

will likely mean a longer-than-average downturn.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.