Green hydrogen has the potential to produce nearly a fifth of total energy demand by 2050

The US Inflation Reduction Act is generally a tailwind for new hydrogen projects

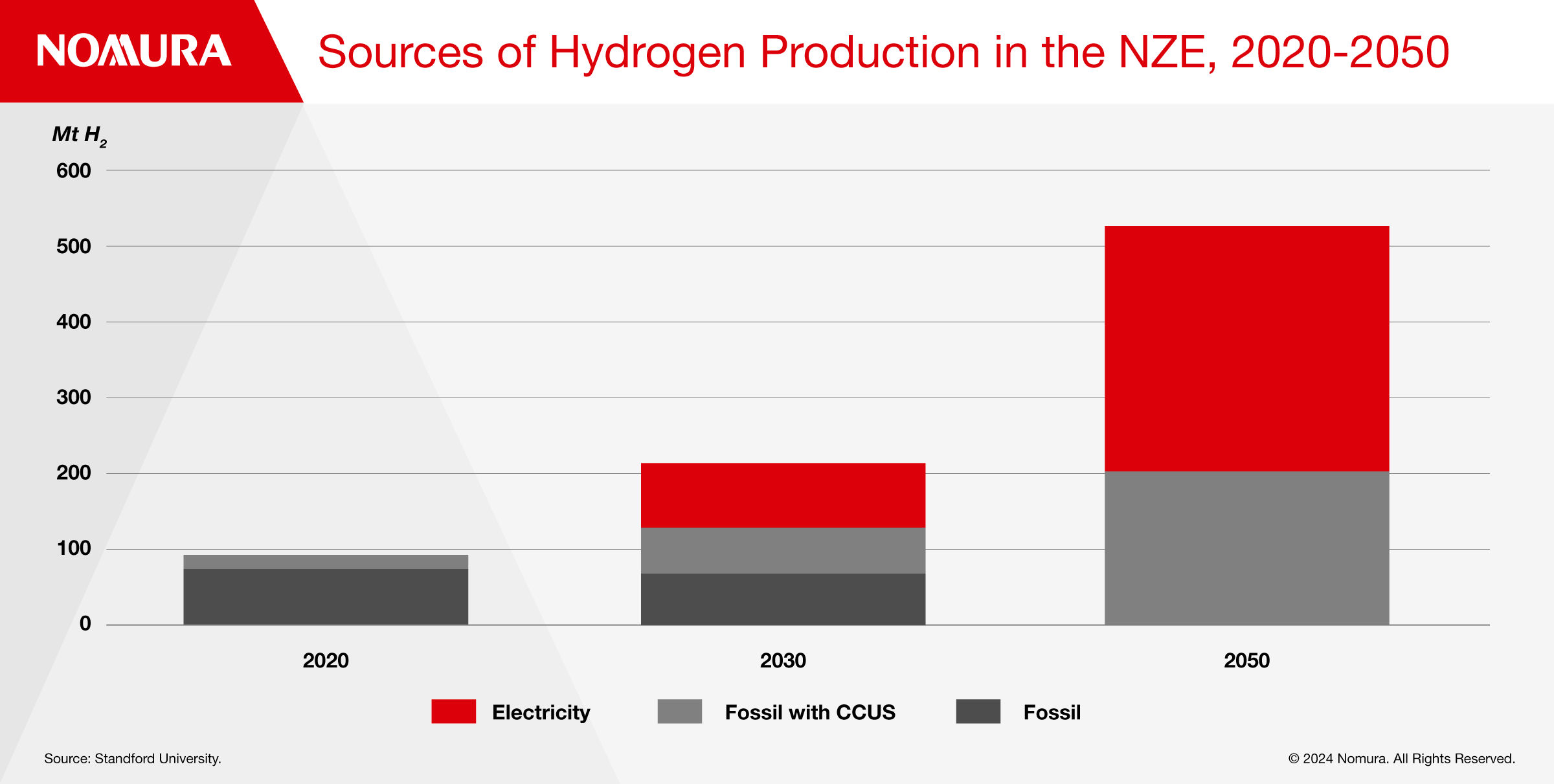

We need ~600 GW of electrolyzers by 2030 to achieve net zero emissions by 2050; last year, we produced ~1 GW globally

Globally, there are about 10 active geological storage sites for hydrogen

Policy support driven by the Inflation Reduction Act is fueling investment in low-carbon hydrogen but storage and electrolyzer challenges mean that it is not a panacea to reduce emissions, according to an expert speaking at Nomura Greentech’s Sustainable Leaders Summit.

More than 1,000 hydrogen projects have been announced across the world, to the tune of $320 billion, the expert who used to work in the oil industry said at the summit, held under the Chatham House Rule. She added that the Inflation Reduction Act has been a key tailwind for investment in the US market with production tax credits (PTC) for clean hydrogen estimated at $13bn until 2031.

The PTC is eligible for “clean” hydrogen, defined as a hydrogen source that delivers at a least 60% greenhouse gas (GHG) reduction relative to today’s incumbent fossil (“grey”) hydrogen. The credit then follows a sliding scale, whereby the higher the GHG reductions, the higher the credit.

The expert said that global greenhouse gas emissions in 2023 stood at 50 billion tons, of which, 13% emanated from the US with the International Energy Agency estimating that hydrogen could cut 60 Gt of CO2 emissions by 2050 making it a part of the solution to decarbonization.

Today, 95% of hydrogen production is from thermochemical processes (coal, oil and natural gas) while only 5% is green hydrogen generated via electrolyzers, which means the technology has a lot of potential.

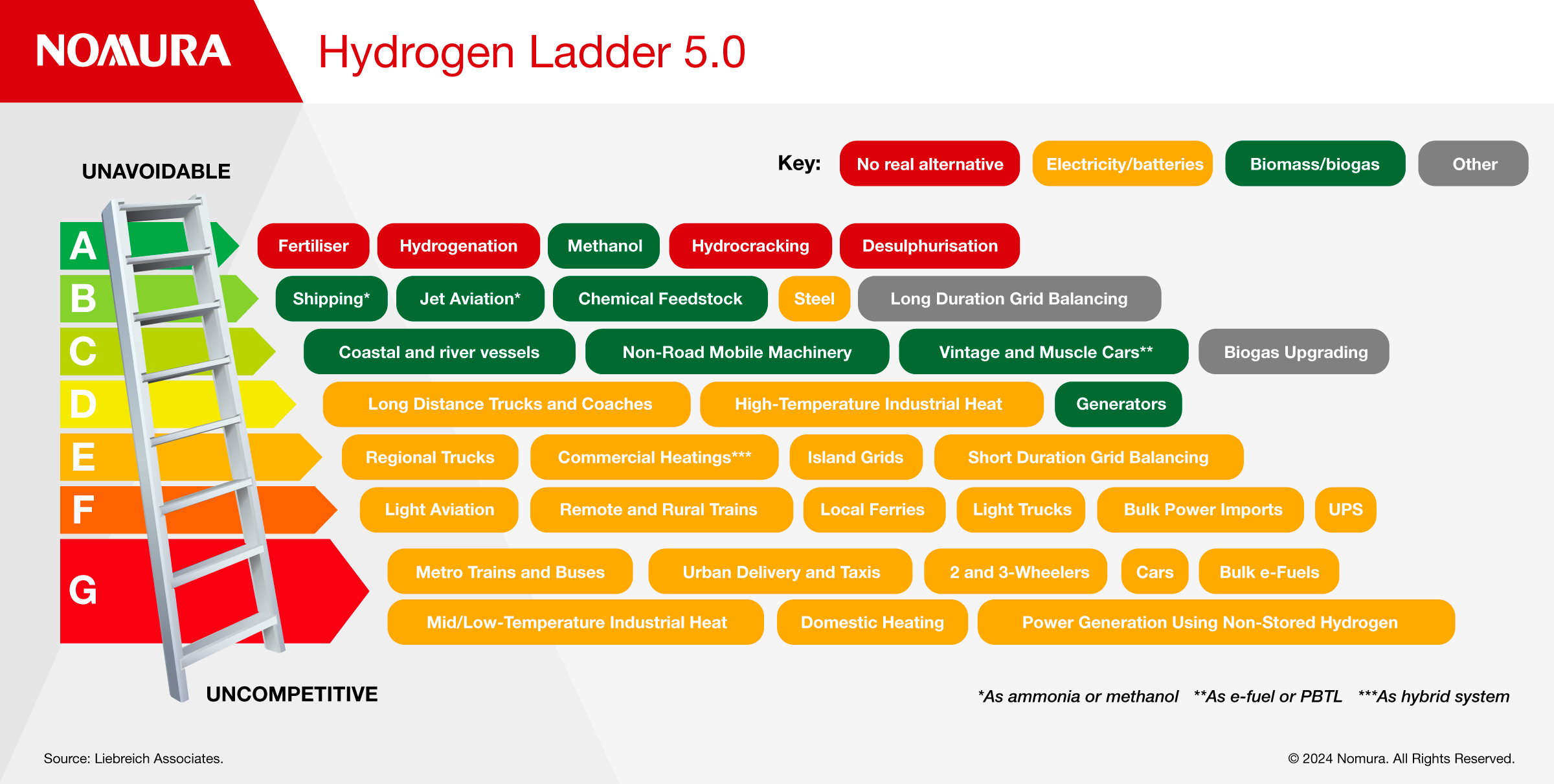

Green hydrogen has many different use cases, and the expert referenced the work of Michael Liebreich who has analyzed where hydrogen adds the most value considering the economic drivers and available alternatives. The top of the ladder includes production of ammonia for fertilizer, methanol, aviation fuel and shipping.

Where hydrogen competes with bio feedstocks and biofuels in shipping and aviation, the bio pathways are great until you realize that collecting used cooking oil from restaurants is very hard to scale, and there is only so much methane from dairies and landfills that can be collected, she said.

“That’s why hydrogen is a prominent contender in many of these applications and often it’s in combination; you’re basically trying to recreate the hydrocarbon chain that we already use.”

The expert said that “interest in hydrogen has gone through the roof” but only 10% of investment so far is at final investment decision stage.

Some of the challenges include the fact that the levelized cost of hydrogen is much higher than its initial production cost.

“It’s $1.10/kg to make it but when I go to the hydrogen refuelling station in California, it’s $15/kg because you have to add transport and storage.”

Making green hydrogen using renewables involves intermittency, so a small amount can be produced in the winter months when solar output is low, with the bulk being made in the spring and summer yet customer demand is all year round, which means storage costs need to be thrown into the equation.

“Storing hydrogen power in batteries has the same problem that we have across the whole energy transition, except that it’s way more expensive to store hydrogen.”

The expert said that storage doubles the production cost of hydrogen. Having a long term 30-year offtake agreement would help to keeps costs in check but there is also a shortage of suitable storage facilities known as salt domes, she said.

The United States stores four trillion cubic feet of natural gas underground and Spindletop in Texas is the largest hydrogen salt dome. Globally, there are only about 10 active geological hydrogen storage facilities, but it might be possible to repurpose depleted oil and gas reservoirs. About 20 more projects are expected by 2030, with the vast majority planning to utilize salt caverns.

The roundtable executives also debated the merits of the IRA’s system of tax credits that rewards the greenest technologies on a sliding scale under the 45V provisions. A separate set of 45Q credits cover carbon capture technologies but project developers cannot take both 45V and 45Q credits for blue hydrogen that use fossil fuels and captures the carbon.

One executive took the view that whenever you deploy new technology, it takes time and effort to perfect it, citing the early combustion engine compared to efficient modern-day cars. “If you don’t start, you’re never going to be able to figure out the optimization path.”

An executive working in carbon capture and storage said that the rules need to build in enough wiggle room to be able to move projects forward in a timely way while attracting capital.

“For a lot of clean energy projects, the government has its foot on the gas and the brake at the same time, and the result is a whole lot of energy going nowhere.”

In response, the expert cited the European approach which uses grandfathering and involves ramping up to stricter environmental standards over time, which gives companies a chance to deploy new technologies sooner while still receiving the benefit of being the first mover.

The expert said that the biggest constraint on a faster rollout of green hydrogen is electrolyzer capacity, which currently stands at about 2 GW globally and needs to reach about 600 GW by 2030 to achieve net zero emissions by 2050.

She said that electrolyzer supply chains were a huge problem as they use a lot of critical minerals like iridium which are in short supply. Additionally, she cited EvolOH as an example of a company that’s putting in place advanced techniques to reduce bottlenecks in the manufacturing process.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.