Euro Area 2025 Outlook – Shifting from Inflation to Growth

The ECB’s focus is shifting from high inflation to worries about anemic economic growth. We increasingly believe the consumer-led recovery is unlikely to materialize. Consequently, we expect the ECB to lower rates to below neutral to support the economy

We expect a slow recovery in economic growth, held back by soft consumption and a structurally weak German economy

US tariffs will be an additional drag on European growth and hit Europe’s already-struggling manufacturing sector

Early German elections could pave the way to some fiscal loosening from Q4 2025, and France is likely to face less fiscal drag than we previously expected, due to political turmoil

Inflation is no longer of concern

In our view, inflation is no longer a concern in the euro area. HICP inflation was sub-2% in September 2024, long before the ECB had expected. Since then, it ticked up to 2% in October and 2.3% in November, though this is solely due to base effects rather than an acceleration in underlying momentum. Services price momentum, on which the ECB has squarely focused for much of 2024, continues to edge lower; it averaged 0.12% m-o-m per month from September to November, much lower than the average of 0.42% per month in H1 2024. We forecast a decline in HICP inflation to below the ECB’s 2% target by spring 2025.

Wage growth is likely to slow

The ECB’s euro area negotiated wage growth series rose to 5.4% in Q3 2024, which is 10-40bp higher than the ECB’s expected range. However, the strength in this print was almost entirely attributable to Germany, which saw the strongest wage growth in more than 30 years. Germany contributed 2.8pp to the headline euro area figure, with the remaining Big 4 contributing only a cumulative 1.3pp. Wage growth in the remaining Big 4 is either moderating or has stabilized at levels consistent with the ECB's target of 2% inflation over the medium term.

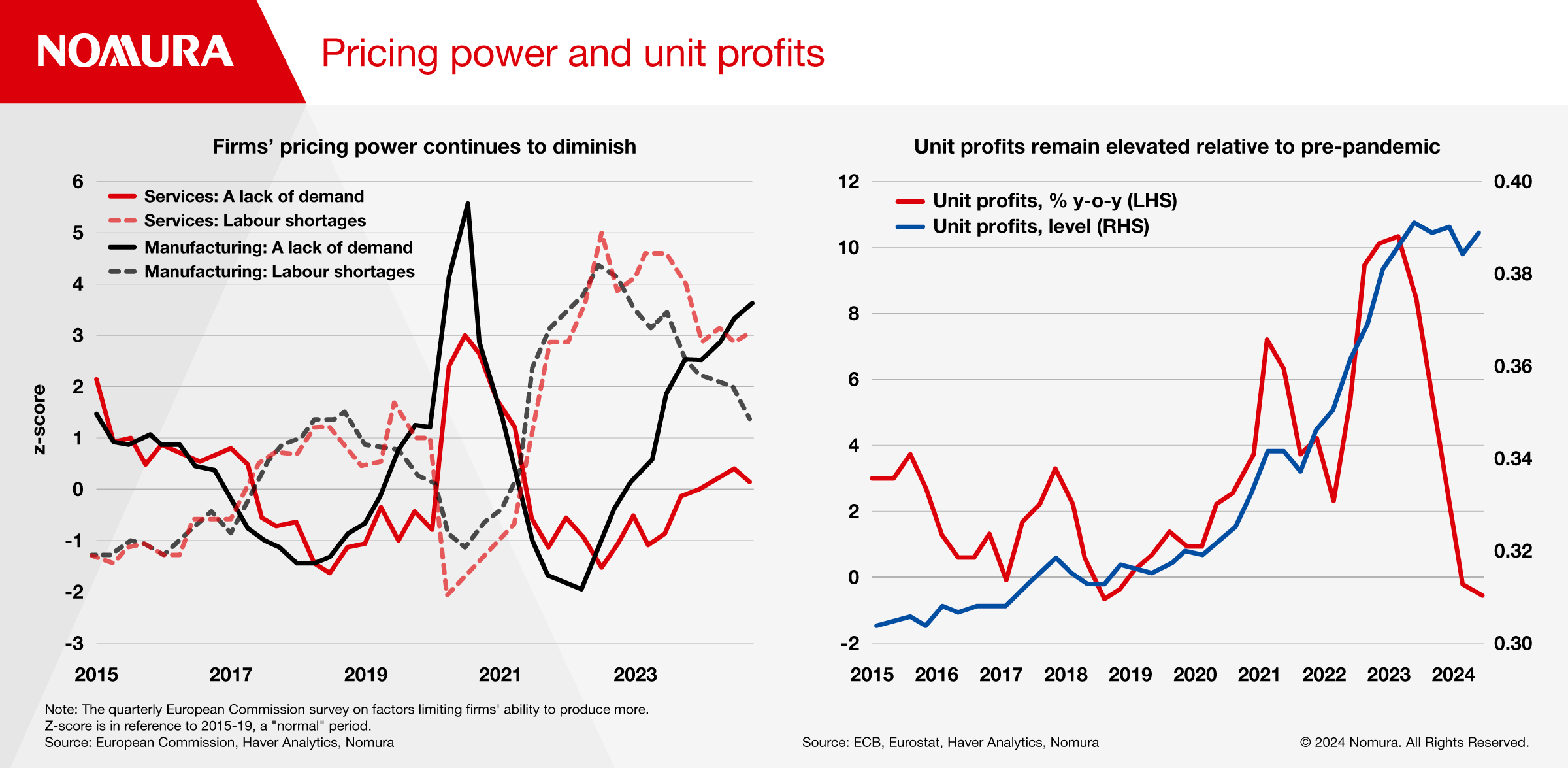

Firms pricing power continues to diminish; Unit profits remain elevated relative to pre-pandemic

Firms’ pricing power continues to diminish

Sufficient demand is a key factor in allowing firms to pass higher input costs on to consumers. The Q4 2024 European Commission survey, shown in Fig. 62, suggests firms’ pricing power has weakened.

This means euro area firms are increasingly likely to struggle to pass higher input costs onto consumers, which may result in consumer inflationary pressures abating further over the coming months. For services firms, they may eventually need to absorb strong wage growth, lowering profit margins. Similarly for manufacturing firms, strong wage growth and rising shipping costs are likely to also hurt profit margins.

US tariffs are likely to be minimally inflationary for Europe

We expect the US to apply blanket 10% tariffs on imported goods following the election of Trump, and we believe the European Commission will retaliate like-for-like, which could mean higher inflation across Europe. However, with manufacturing firms' pricing power having greatly diminished, firms will likely be compelled to absorb some of these higher costs, which in turn may result in lower profits, some firms shuttering and unemployment rising. This effect could weigh additionally on growth. With the euro area imports from the US equaling just over 2% of GDP, 10% retaliatory tariffs could add 0.1pp to the GDP deflator. Hence, we believe the direct impact of US tariffs on Europe’s inflation will be minimal, particularly when compared with the impact on its growth.

An anemic economic outlook

We expect a slow recovery in economic growth, held back by soft consumption and a structurally weak German economy. US tariffs will be an additional drag on European growth and hit Europe’s already-struggling manufacturing sector. We forecast euro area GDP growth to accelerate to 1.1% in 2025 and 1.3% in 2026, from 0.8% in 2024 .

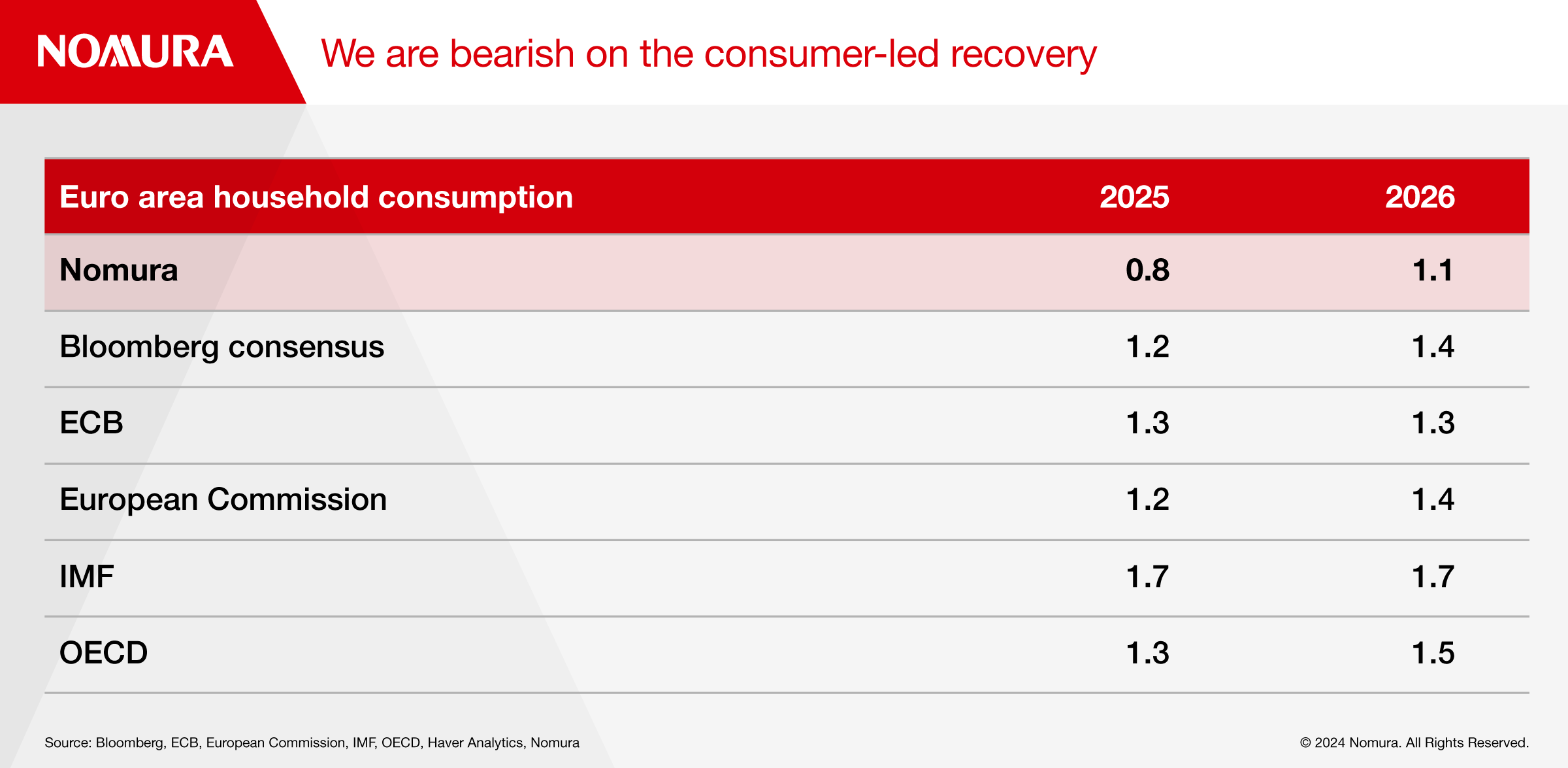

We are bearish on the consumer-led recovery

Goodbye consumer-led recovery

Official institutions (ECB, IMF etc.) expect a consumer-led recovery in 2025 due to:

Robust real wage growth;

Some drawdown of household savings; and

An easing of financing conditions. They forecast euro area GDP growth will accelerate to 0.4-0.5% q-o-q by early 2025.

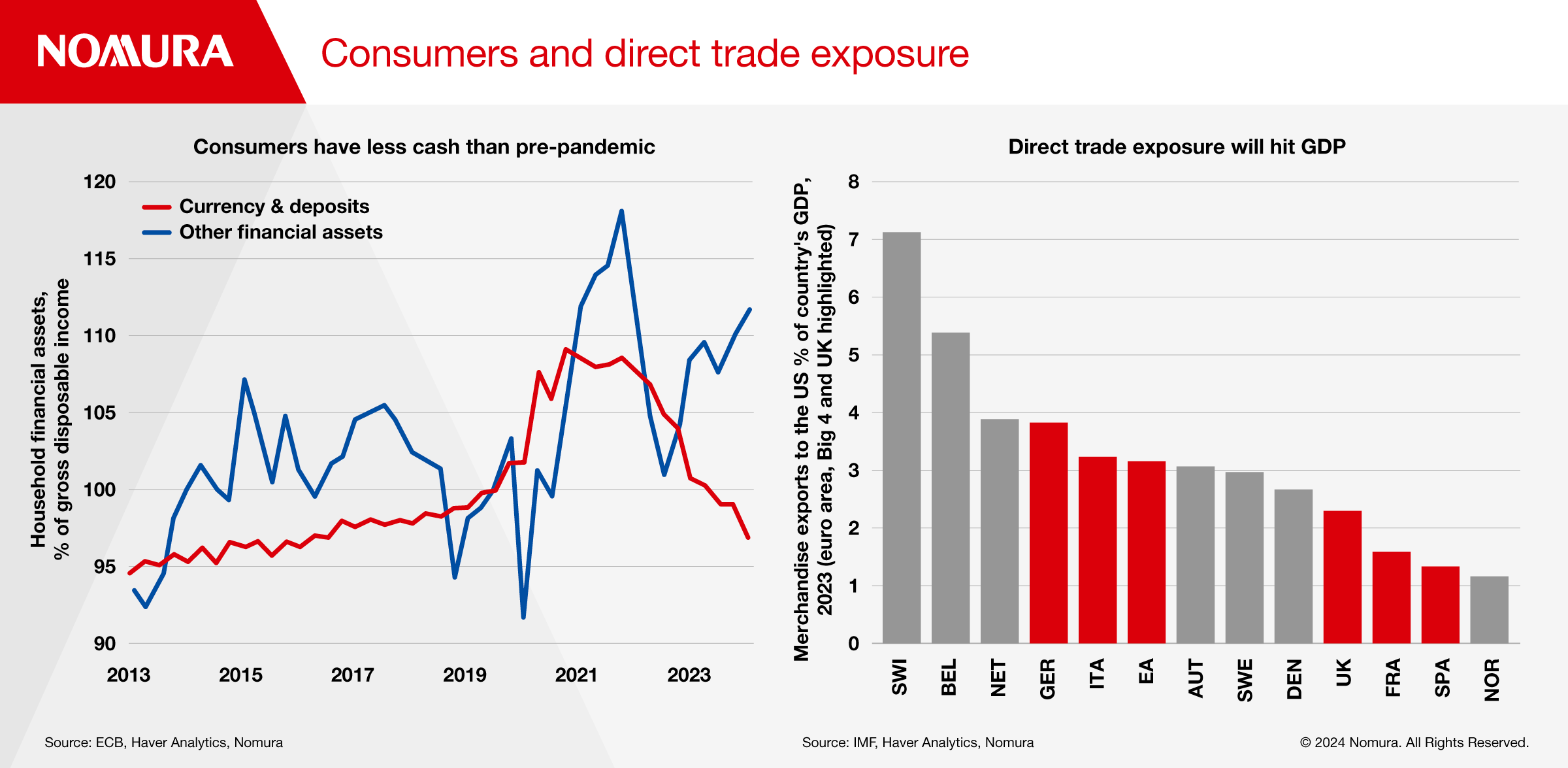

We are more bearish on the euro area’s potential consumer-led recovery and forecast household consumption growth of 0.8% in 2025 and 1.1% in 2026. Real wage growth is slowing more sharply than the ECB had expected, and households have less available cash than before the pandemic (Fig. 66).

Fig. 67 shows Europe’s exposure to goods trade with the US with Trump’s potential tariffs likely be focused on goods (not services) imports to the US. Germany looks most vulnerable as it exports more goods as a percent of GDP to the US and is more exposed to China, where growth could be damaged by substantial US tariffs.

Consequently, we expect US tariffs to lower euro area GDP growth by a cumulative 0.3pp over 2025 and 2026.

Germany faces structural issues

Beyond recent cyclical weakness in Germany, we expect its economy to stagnate as its issues are largely structural. Hence, we think Germany’s GDP growth is unlikely to return to its pre-pandemic trend by the end of our forecast horizon in Q4 2026.

Important adverse factors in Germany include:

(i) greater exposure to a weakening China with its own structural headwinds;

(ii) more pronounced exposure to a global manufacturing downswing, as well as increased competition from China and a shift to electric vehicles; and

(iii) deteriorating demographics, with the biggest expected rise in dependency ratios among the G7 in the next decade and a shrinking population.

All of these factors suggest little is required in the way of cyclical weakening in Germany to produce a recession.

Consumer have less cash than pre-pandemic; Direct trade exposure will hit GDP

Cutting rates to below neutral to support the economy

We forecast 125bp of further rate cuts, with a 25bp cut per meeting in H1 2025 and a final 25bp rate cut in September 2025. Ultimately, we believe the ECB will be compelled to cut rates to below neutral (we see neutral as 2-2.5%) to support the economy. We expect the ECB to cut the depo rate to 1.75% by September 2025.

UK: Cutting to the top end of neutral

We expect UK economic growth to slow in the coming quarters before picking back up towards trend later in 2025. The government’s latest budget is growth-positive, but potential US tariffs on the UK would have the opposite effect. Inflation could be temporarily boosted in the event of tit-for-tat tariffs, but we think the more important trend of slowing domestically generated inflation will remain a key theme for 2025 and beyond. Inflation is likely to rise in the near term due to base effects and budget measures but should be sustainably back at target in H1 2026. Unemployment could rise further in response to near-term sub-trend growth, but only modestly, in our view.

Slowing growth to slowly recover

GDP now stands at 3% above its pre pandemic peak, with consumer spending also now back above its Q4 2019 level (before the revisions, it was below). Still, UK GDP and its various expenditure components have generally underperformed those of other peer group countries – particularly when it comes to consumer spending and trade.

We expect growth to run at a below-trend (and below-consensus) rate of 0.2% q-o-q in Q4 2024 and Q1 2025 before nudging up to 0.3% q-o-q thereafter, ultimately settling at 0.4% q-o-q at the end of our forecast horizon in H2 2026.

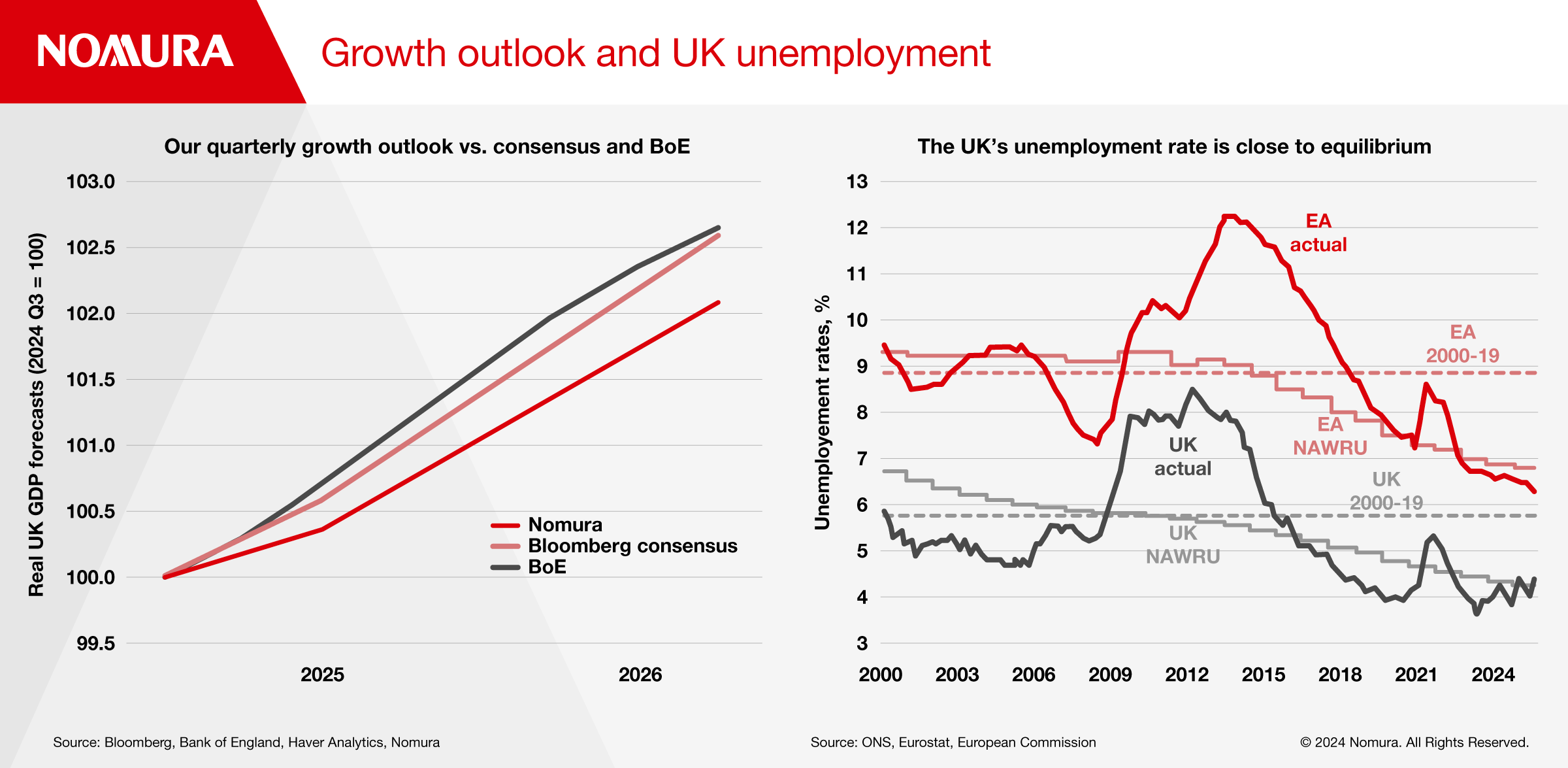

How our forecasts compare

Fig. 76 shows that our growth forecasts are weaker versus both consensus and the Bank of England’s view for two main reasons: i) we incorporate the recent weaker survey evidence, in particular the fall in the November PMIs, and ii) while the BoE includes a material upside effect from the fiscal loosening contained in the latest budget, it does not include an offsetting Trump tariff effect (which our numbers do.

Our quarterly growth outlook vs consensus and BOE; The UK's unemployment rate is close to equilibrium

While we see consumer spending supporting GDP growth in coming quarters, aided by falling interest rates, a still-robust labor market and rising confidence, its contribution might be limited by:

i) our view of slowing nominal wage growth;

ii) inflation turning back up in the near term due in part to higher energy prices;

iii) confidence remaining below its pre-pandemic average; and

iv) the former build-up in cash savings having been eroded (relative to incomes).

Loosening, not loose

The unemployment rate remains low at 4.3% – a little under the Bank of England’s view of equilibrium (4.5%). Together with vacancies – which, relative to unemployment, have fallen to levels similar to where they stood pre pandemic – this suggests the labor market is loosening, but is still not loose in absolute terms. Based on our view of a period of modestly sub-trend economic growth in the near term, we expect unemployment to rise only a touch, which is not that different from the BoE view.

Making progress on inflation

The latest UK inflation print rose due to energy price base effects, rather than any material strengthening in consumer price momentum. As such, we think the Bank of England will look through this and instead focus on developments in service prices and underlying monthly price momentum.

Services inflation remains elevated at 5% y-o-y; while that did not surprise the Bank of England, which forecast this in its November Monetary Policy Report, it does remain too high for comfort/achieving the 2% CPI inflation target.

We expect headline inflation to rise further in the near term, peaking at a quarterly average rate of around 2.8% in Q1 2025 mainly due to service and energy price annual base effects, and slowly falling to just over 2.5% by end-2025.

We continue to think the Bank of England will cut interest rates at a quarterly pace, 25bp at each Monetary Policy Report, until reaching 3.50% early in 2026.

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.