Resilience of global M&A

Global M&A saw a marked increase in the wake of the pandemic, but is this rise here to stay, and if so in which sectors?

This article was produced in collaboration with

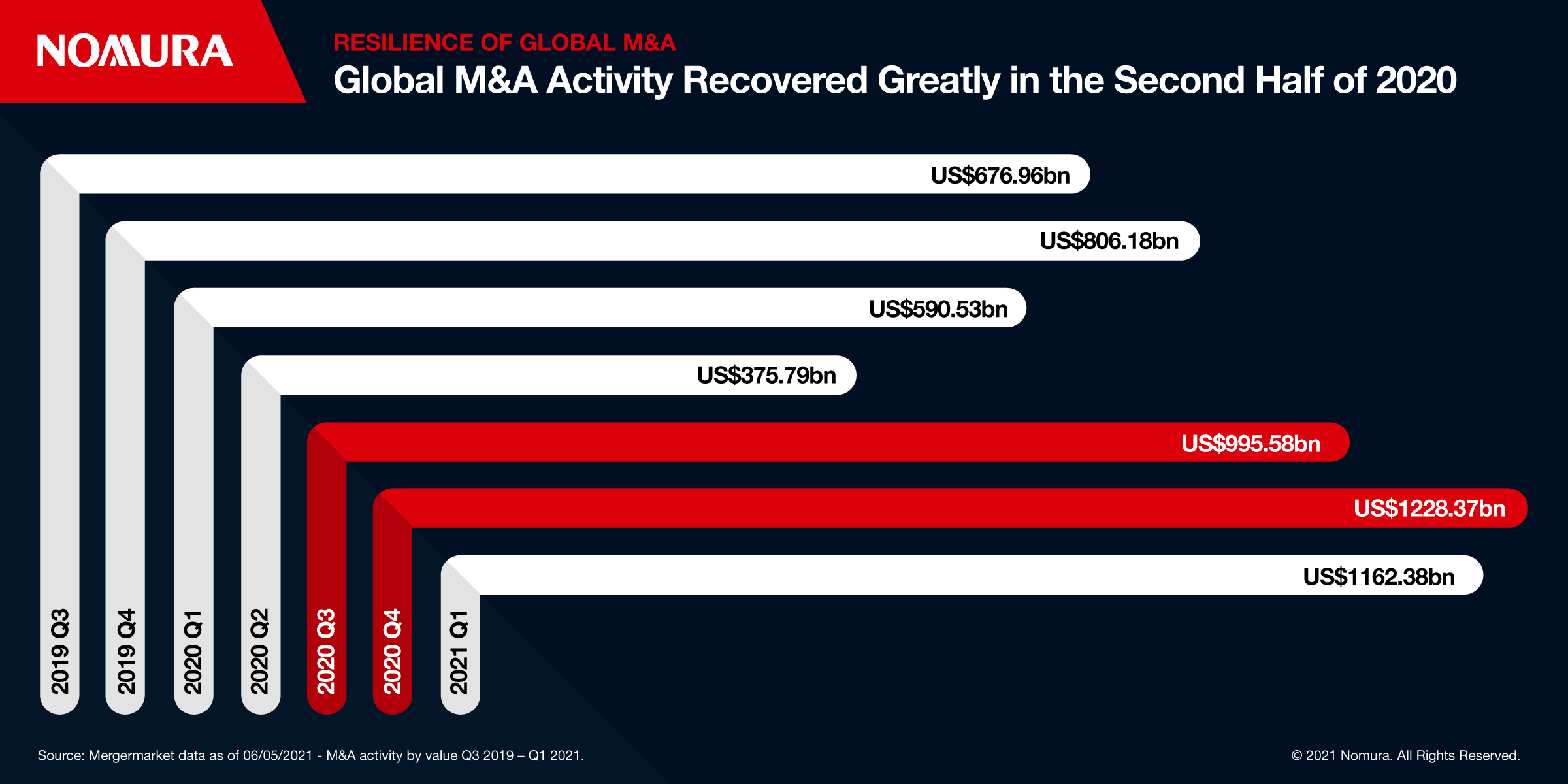

Following a sharp fall in early 2020 due to the pandemic, M&A activity rebounded robustly later in the year and looks set to continue on that course through 2021. Cross-border deals have been particularly resilient, and the trends of digitalization and the push for sustainability, combined with some cash-rich corporates and the rise of SPACs, will likely help maintain that momentum.

Companies that benefited during the pandemic, led by tech firms, now have more financial firepower at their disposal. And even in sectors negatively impacted by the shifts in the economy and consumer behavior, there is potential and the need for consolidation and restructuring-driven deals. Meanwhile, shareholder activism is increasing pressure on underperforming companies to deliver more value.

“Financial institutions are stronger due to new regulations introduced after the global financial crisis,” notes Shinsuke Tsunoda, Nomura’s Global Head of M&A, meaning that credit has been available for deals even during the pandemic.

In terms of secular trends, the growing wave of digitalization and the push to decarbonize will be major global disrupters in the years and decades to come. As new technology develops, business models transform and new sectors emerge, M&A will be a pivotal part of those processes.

“The emergence of green tech, which spreads across multiple sectors, will continue to be a driver of M&A,”

Two major semiconductor deals, Japan’s Renesas Electronics €4.9 ($5.97) billion takeover offer for UK chipmaker Dialog Semiconductor, announced in February, and Taiwan’s Global Wafers bid to acquire German counterpart Siltronic AG for an equity value of €4.35 ($5.3) billion in December, point to the appetite for acquisitions in the tech sector. Both the Asian acquirers were advised by Nomura, and many corporates in the region, which has been hit relatively lightly by the pandemic, have the incentives and the means to be active players.

“Japanese clients have a compelling rationale for M&A, they are faced with very slow or no growth in the domestic market. So it’s a natural choice to go outside, to go abroad and buy a business where growth and demand is higher than in Japan,”

In addition, Japanese companies are sitting on a record cash pile and are being pushed by shareholders and the country’s corporate governance code to deploy capital more efficiently.

“Shareholder activism has also been a driving force in the US and is becoming increasingly important in Europe and Asia. This has brought pressure on underperforming companies to sell assets, and created opportunities for our clients to buy businesses being sold off,” says Rouner.

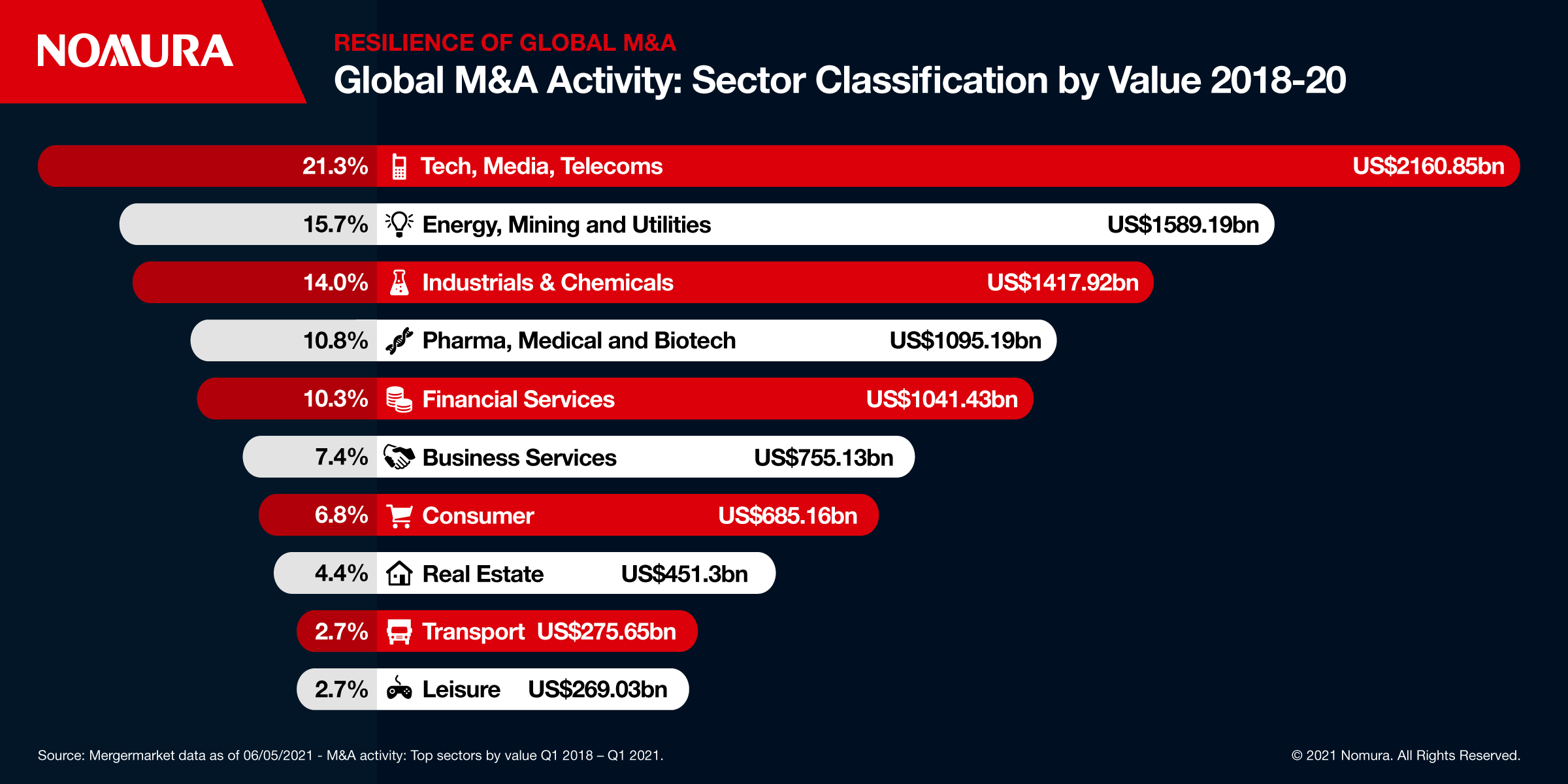

That was the case in 7-Eleven’s $21 billion acquisition of the Speedway chain of convenience stores from Marathon Oil, where Nomura advised 7-Eleven and its Japanese parent company in one of the largest global deals last year. Under pressure from activist investor Elliott Management to restructure, Marathon announced plans to spin Speedway off to its shareholders but accepted a cash offer from 7-Eleven to acquire Speedway instead. Although Tech M&A has been grabbing much of the attention, M&A activity is broadly based across a wide range of sectors.

“With valuations of tech assets hitting record highs, focus may shift to out of favor sectors such as construction, building materials, and chemicals, as well as to recovery plays in pandemic-hit industries like leisure, travel, and retail,”

SPACs remain focused on emerging technology, though the disruption they have brought to the M&A space in the US may reach other regions.

“The London Stock Exchange is looking at how to capture SPAC activity, and the growth of SPACs may spread to Europe and Asia, in the way private equity and shareholder activism has done, further down the line. In terms of potential downside risk for global M&A, there are a few potential clouds on the horizon,” points out Hayward-Cole.

“Central banks have been printing money as if there’s no end to it on and off since the global financial crisis. That has to stop at some point and people forget that. There is a world out there where credit becomes more expensive,” says Hayward Cole. “There is a whole generation of business owners and managers who haven’t operated in inflationary conditions.”

Though as the pandemic has shown, even a dramatic shift in the landscape doesn’t sound the knell for acquisition activity. “Uncertainty can also give companies reasons to do deals,” points out Tsunoda.

As the global economy emerges from the pandemic, a range of realignments, not the least of which will be digitalization and decarbonization, appears inevitable. And M&A looks certain to play a significant role in those seismic shifts.

Read the article on Reuters.com here.

Contributor

Shinsuke Tsunoda

Senior Managing Director, Global Head of M&A, Head of Solution Business of Japan

Guy Hayward-Cole

Chairman of Technology, Media & Services, Head of EMEA Advisory

Jonathan Rouner

Vice Chairman, International Head of M&A,

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.