China: How the North/South Divide Highlights the Credit Risk Disparity

The widening north/south divide could result in a vicious cycle of rising defaults and slower growth in northern China. Though we do not expect a national crisis, markets should be prepared for more defaults.

- Understanding the north/south divide and its implications is crucial to risk analysis.

- We expect the economic disparity between China’s northern and southern regions to worsen further as policymakers rein in property market financing and enact carbon neutral environmental policies.

- The widening north/south divide could result in a vicious cycle of rising defaults and slower growth in northern China. Though we do not expect a national crisis, markets should be prepared for more defaults.

- Beijing is unlikely to ease restrictions on property market financing, but may adjust any overly harsh antipollution measures, and might step up fiscal transfers to northern China.

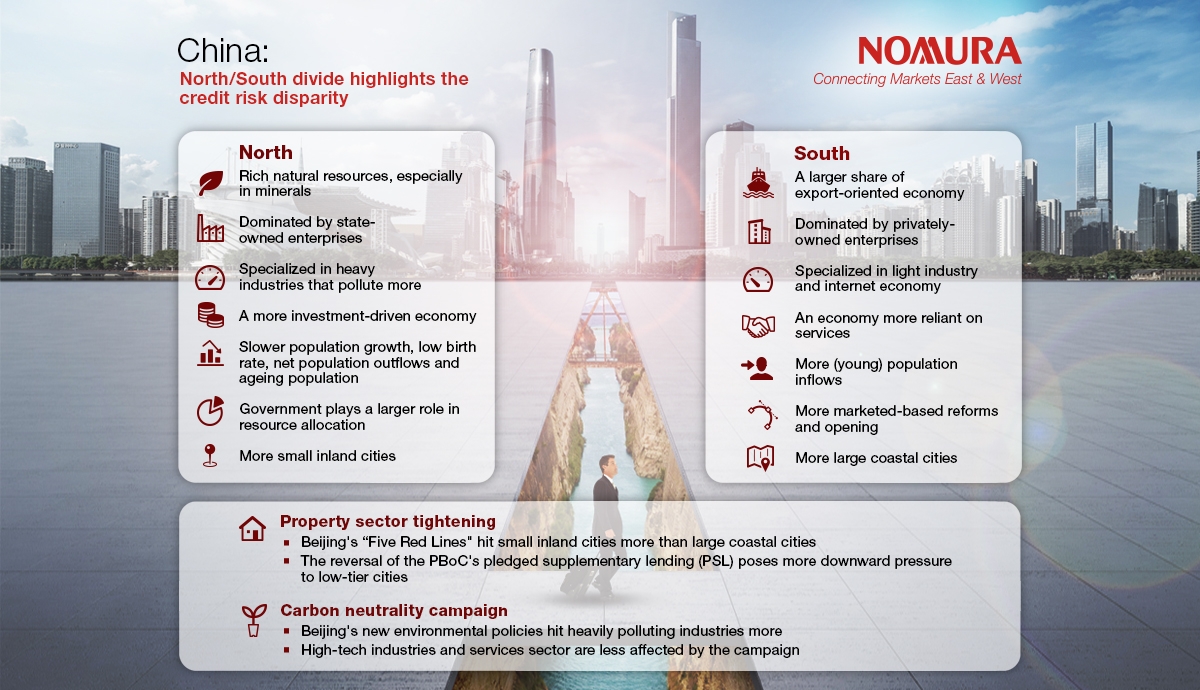

China’s onshore debt market has experienced a rapid rise in defaults in recent quarters, while offshore dollar bond defaults were also near record highs. China’s north/south divide, which refers to the economic disparity between China’s northern and southern regions, has become more evident in recent years by these delinquencies and repayment pressures in debt markets. We expect this divide to worsen as policymakers rein in property market financing and enact carbon neutral environmental policies, which could result in a vicious cycle of rising defaults and slower growth in northern China.

The economic gap between northern and southern China has increased significantly over the last decade, with the southern region benefiting from its dominance in exports, the internet boom and more market-based reforms. On the other hand, the resource-rich northern area has suffered from slowing fixed asset investment, declining commodity prices, and an aging population due to strict implementation of the one-child policy over the last two decades of the 20th century.

Before 2012, the divide was not a big issue, with the southern region benefiting from booming exports and robust light industries, and northern part profiting from resource-focused and infrastructure-led investments. Since then, economic drags felt across the country due to industrial overcapacity, debt build-up, a cooling property sector and the anti-corruption campaign, meant northern China had to bear the brunt as it was more heavily exposed.

Unsurprisingly, Covid-19 also contributed to the widening of the divide. Although all of China’s economy was severely affected by the pandemic, southern China fared better than its northern counterpart. As home to many large internet companies including Alibaba and Tencent, the southern China benefited from the social distancing-driven boom of the internet economy. Additionally, during the country’s rapid economic recovery, which began in Q2 2020, exporters in the region were able to stage a sharp turnaround towards the end of 2020.

The disparity is expected to widen for two reasons:

- Beijing’s tightening measures on the property sector will likely have an outsized effect on North China: Due to rising concerns over a property bubble and consequent financial risks, Beijing has maintained its hawkish stance on the property sector. North China has lagged well behind the southern area in economic and population growth over the past decade, and a number of provinces in the north of China have experienced net population outflows. As property demand is a function of the economy and population, developers could allocate more available funding to the south, putting pressure on land sales revenues for local governments in northern cities. For homebuyers, considering the limited supply of mortgage financing, some may choose to buy homes in South China in anticipation of migrating there.

- North China could be more deeply affected by Beijing’s new environmental campaign: In September 2020, China committed to reaching peak CO2 emissions before 2030 and carbon neutrality by 2060. A rush by ministries, local governments and corporates to cut carbon emissions could hit heavy industries such as producers and processors of steel, aluminum and other raw materials, which are concentrated in the northern region. This could impact the public finances of some of the northern cities disproportionately, adding to credit defaults risks.

For bond investors, risk premia for debt issued in northern China are rising rapidly, and investors will need to closely monitor markets as these risks unfold. Treating China as a uniform whole is not a sound approach to credit pricing, and understanding the north/south divide and its implications is crucial to risk analysis. Healthy macro data at the country level can conceal the magnitude of the divide between the two regions.

The impact of the north/south divide on policymaking:

- Regarding carbon peak/neutrality environmental policies, Beijing may have to correct/ease some of the overly harsh measures imposed on polluting companies, especially on producers of base materials in North China, in H2 2021 and 2022.

- We do not expect any significant easing of the tightening measures on property markets, even though several lower-tier cities in North China will likely start to feel the financial pinch very soon.

- On macro policies, we expect Beijing to wholeheartedly stick to its commitment to make no sharp policy shift this year, and step up fiscal transfers to North China.

- When defaults do occur, we would expect Beijing to take a cautious case-by-case approach in determining whether to bail out these companies.

For further insight into China’s credit risk disparity, read our full report.

Contributor

Ting Lu

Chief China Economist

Lisheng Wang

China economist

Disclaimer

This content has been prepared by Nomura solely for information purposes, and is not an offer to buy or sell or provide (as the case may be) or a solicitation of an offer to buy or sell or enter into any agreement with respect to any security, product, service (including but not limited to investment advisory services) or investment. The opinions expressed in the content do not constitute investment advice and independent advice should be sought where appropriate.The content contains general information only and does not take into account the individual objectives, financial situation or needs of a person. All information, opinions and estimates expressed in the content are current as of the date of publication, are subject to change without notice, and may become outdated over time. To the extent that any materials or investment services on or referred to in the content are construed to be regulated activities under the local laws of any jurisdiction and are made available to persons resident in such jurisdiction, they shall only be made available through appropriately licenced Nomura entities in that jurisdiction or otherwise through Nomura entities that are exempt from applicable licensing and regulatory requirements in that jurisdiction. For more information please go to https://www.nomuraholdings.com/policy/terms.html.